Testimony: New York City’s Housing Emergency

Oksana MironovaSamuel Stein

Thank you to the New York City Council’s Committee on Housing and Buildings for holding this hearing on the 2023 Housing and Vacancy Survey (HVS), the determination of a housing emergency, and the continuation of rent stabilization and rent control.

Our names are Oksana Mironova and Samuel Stein and we are senior policy analysts at the Community Service Society of New York (CSS), a leading nonprofit that promotes economic opportunity for all New Yorkers. CSS uses research, advocacy, and direct services to champion a more equitable city and state.

A Public Emergency

New York defines a housing emergency by a clear threshold: a vacancy rate below 5 percent for rental housing in habitable condition. The Select Initial Findings of the 2023 Housing and Vacancy Survey show that New York City remains deep in such an emergency, not only justifying the continuation of rent control and rent stabilization, but clarifying the very connection between low vacancy and the need for rent regulation.

The 2023 HVS shows that New York City’s net rental vacancy rate is 1.41 percent, one of the lowest on record. It is a steep fall from 2021’s 4.54 percent rate, one of the highest on record. Such an extreme swing denotes extreme times when the need for a regulatory framework that balances the scales between tenants and landlords is most needed. This swing captures turbulence in the housing market, as New York City pulled out of the most extreme phase of the Covid pandemic, and a remarkable 22 percent of households moved into their current home (including both intra-city moves and moves from elsewhere).

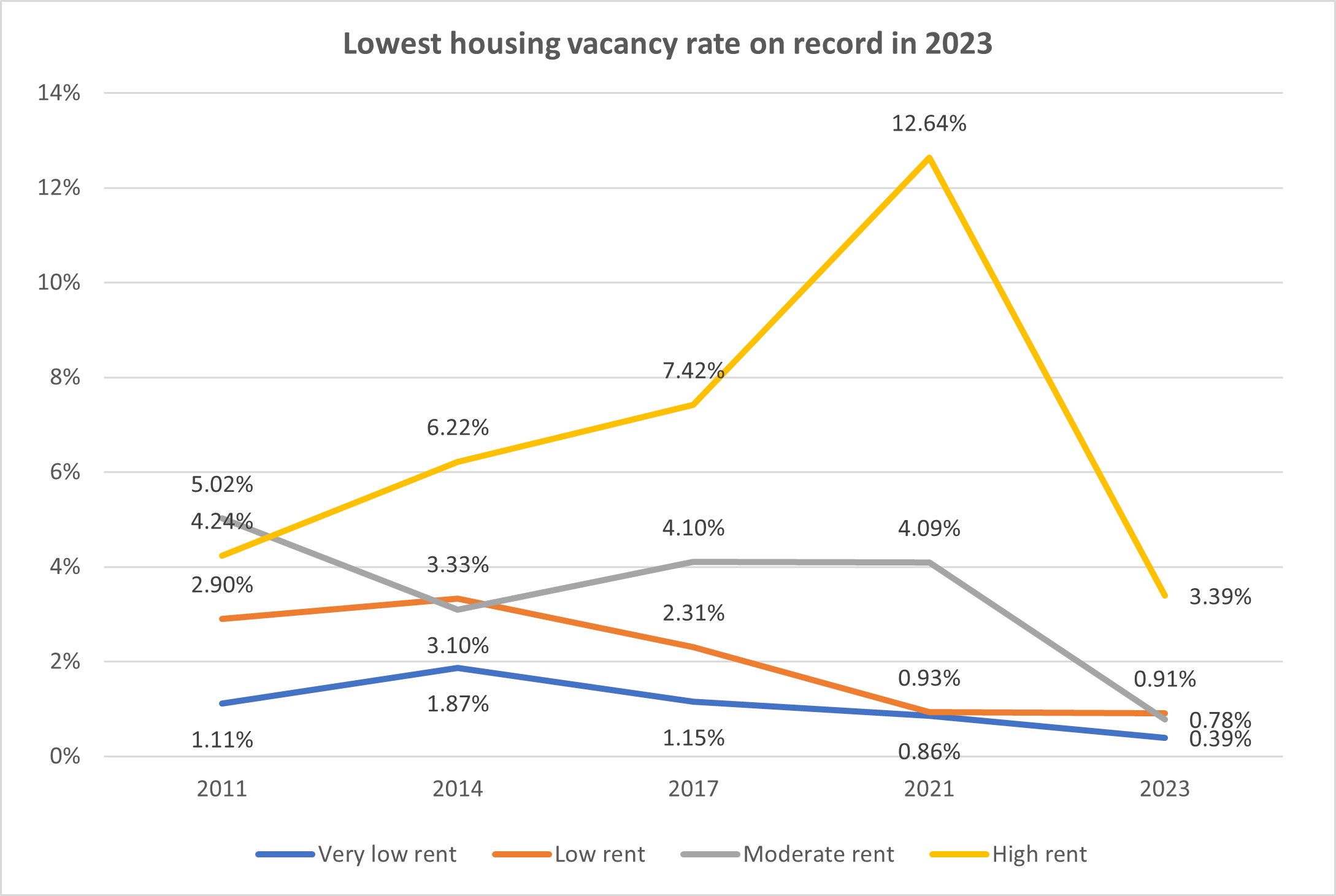

The Fewest Apartments with the Lowest Rents

The survey also highlights that within that overall tight housing market, available low-cost housing remains the scarcest. The vacancy rate for apartments at the bottom quartile of the rental market (what the survey calls “very-low rent” apartments) is virtually non-existent at 0.39 percent. Shockingly, the vacancy rates for the next two quartiles (“low rent” and “moderate rent” apartments) are also below 1 percent, at 0.91 percent and 0.78 percent respectively. And while the vacancy rate for the top quartile (“high rent” apartments) has dropped dramatically since its historic high last year, by comparison to the rest of the market it soars at 3.39 percent. This trend of rent-polarized vacancy rates is a clear trend that has developed over time, but the convergence of the bottom three quartiles at extremely low vacancy is a new phenomenon. (See chart below.)

The 2023 HVS reports that not only is vacancy is essentially non-existent among low-rent units, but New York City has lost such apartments altogether at an alarming rate. Between 1993 and 2023, New York City lost over 600,000 units with rents at or below $1,500 (adjusting for inflation). Meanwhile, we have added 75,000 units with rents over $5,000.

As a result, the HVS finds that there were less than 5,000 apartments available in the city for households making less than $50,000 – a population that, according to the 2022 American Community Survey includes over 1.17 million households, or 36 percent of the population. Meanwhile, there were more than 33,000 apartments available to the 16 percent of New York City Households (512,267 households) who earn more than $200,000 a year.

Low Vacancy Rate Demands Strong Regulation

New York’s rent control and rent stabilization laws are backed by a clear premise, which this year’s HVS clearly demonstrates: when vacancy rates are low, individual tenant households lack market power.

While many Councilmembers today are tenants themselves, but for those who are not: imagine that you are a renter, that we don’t have rent regulation, and that housing conditions are as reported in the most recent HVS. Your landlord raises your rent above what you can afford to pay, simply because they can – they think someone will pay more for the space, and they want higher profits. Meanwhile, conditions in your apartment and your building keep getting worse, so you know the money isn’t going toward repairs and investments. What do you do? In such a tight housing climate, you can’t exercise your power as a housing “consumer” and pick up and leave, because there are so few places available – and particularly so few that you can afford. Instead, you’re forced to stay put, watch your rent burden grow, and suffer through bad conditions lest you speak up and your landlord retaliates by refusing to renew your lease. It’s that, doubling up with family or friends, or homelessness.

This is the legal justification for rent control and rent stabilization. When there is such an extreme imbalance in market power between landlords and tenants, it is incumbent on the state to step in and prevent the most severe forms of exploitation. Rent stabilization (in 996,600 apartments) and rent control (in 24,020 apartments) keeps landlords from exploiting this housing crisis and gives tenants the legal backing to push back against deferred maintenance and neglect with the confidence that their lease will be renewed at a rate allowed by the law.

A Note on the Housing Stability and Tenant Protection Act (HSTPA)

This is the second RSL hearing since the Housing Stability and Tenant Protection Act (HSTPA) of 2019 went into effect. Before the HSTPA, when a tenant moved out, rent stabilized apartments were eligible for a 20 percent as-of-right increase and unchecked and often inflated increases resulting from Individual Apartment Improvements. Apartments that reached a legal rent of $2,816 were eligible for decontrol. Unscrupulous landlords developed business practices contingent on these loopholes, all geared toward increasing the net operating income of their stabilized properties, which allowed them to overleverage their buildings with more and more debt. Conditions for tenants got so bad that the city and state were forced to sharpen their definitions of tenant harassment.

Lenders were complicit in these practices. As the Association of Neighborhood and Housing Development’s (ANHD) Equitable Reinvestment Committee (ERC) has shown, some multifamily lenders’ core business practices relied on “making multifamily loans to bad acting landlords.” For example, “year after year, building after building, Signature Bank consistently made multifamily loans that were speculative and underwritten to practices of displacement, harassment, or building neglect.”

If rent stabilized building values are now falling, it’s because the market is resetting to the prices associated with the rents in the buildings – no more, no less. If previous rounds of sky-high valuations were based on dreams of ever-rising rents and net operating income, today’s are based on realistic assessments of what tenants pay each month according to the law.

At the same time, the reality is that there are financially distressed, rent stabilized properties on the market today. As this committee considers the implications of the 2023 HVS and the RSL, we hope that it also engages with the opportunity to rescue overleveraged properties and turn them into permanently affordable housing. The city could intervene by funding Neighborhood Pillars, a program created by the de Blasio administration in the long shadow of the 2008 foreclosure crisis. It can also pass the Community Opportunity to Purchase Act (Int 1977), to establish a legal framework for the transfer of buildings from distressed private ownership to public, tenant community-controlled social housing.

Today, we strongly urge the council to determine that a public emergency requiring rent control in the City of New York continues to exist and will continue to exist past April 1, 2024, and that the Rent Stabilization Law of 1969 be continued.

If you have any questions or want to discuss further, please reach out to us at omironova@cssny.org and sstein@cssny.org.