How Social Is That Housing?

Oksana MironovaThomas J. Waters

While social housing is a new term in the U.S. policy landscape, existing affordable housing models like public housing and limited equity cooperatives incorporate aspects of the three primary goals of social housing: insulating housing from market forces, promoting social equality, and enabling residents to exercise democratic control over their housing. To truly live up to this ideal standard, these housing types would require a large increase in funding and a broader political re-orientation toward “housing in the public interest.” Nonetheless, a new statewide commitment to social housing, as called for by the Upstate-Downstate Housing Alliance, would not have to start from scratch.

In the second part of our series, we explore existing housing models in New York City in relation to social housing, ranking them using its three different dimensions:

| Decommodification measures a housing model’s vulnerability to real estate market pressures. A housing model that is highly decommodified is more likely to meet the social housing goal of permanent affordability. | |

| Social equality illustrates a housing model’s promotion of equal status among its residents and between its residents and non-residents, including racial and economic integration. | |

| Resident control explores the level of meaningful influence a housing model’s residents have over decision-making and governance. |

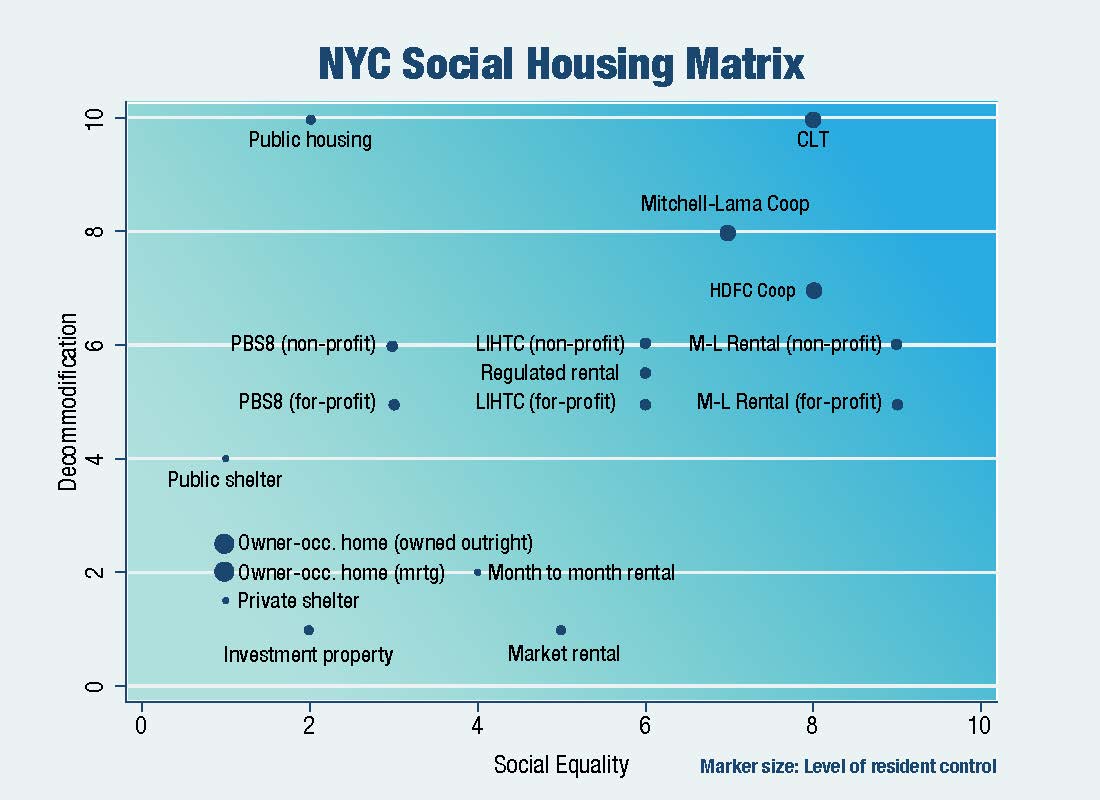

The social housing matrix ranks New York City’s major housing types along three scales: decommodification, social equity, and resident control. Housing types in the upper right corner of the matrix with larger markers exhibit the most social housing qualities; those found in the bottom left corner with small markers exhibit the least.

Owner-Occupied Home

Decommodification: Low

Social equality: Low

Resident control: High

There are approximately 1M owner occupied homes in New York City, making up about 30 of the overall housing stock. Homeowners (including single family, condo, and coop) have the greatest level of control over what their living space looks like, how long they live there, and what they use their property for. They also have the right to sell the property for whatever the market will bear, scoring low on decommodification and high on resident control.

Owner-occupants generally use their homes day to day and are therefore not solely interested in maximizing the return on their investment. Owner-occupied homes are therefore less commodified than market rentals or investment properties. At the same time mortgaged homeowners often have less control over their housing than owners who own their homes outright. An owner’s ongoing need to service their mortgage increases the ability of the market to overrule their preferences about the use of their housing.

Owner-occupied homes score low on social equality because many policies that helped develop the homeownership market in the U.S. are linked to racial exclusion and segregation. Further, it is the form of housing that is imbued with the highest status, as compared to other tenure types.

Community Land Trust

Decommodification: High

Social equality: High

Resident control: High

Community land trusts (CLTs) are nonprofit, democratically governed organizations that steward land to meet community needs. CLTs strive to promote community control and ensure permanent affordability. There are two CLTs in New York City: one in Cooper Square and one in East Harlem, both developed using city-owned property and sustained with long term rental assistance, and about a dozen nascent CLTs in formation across the five boroughs.

Community land trusts (CLTs) score high on decommodification because they are designed to minimize market pressure on land costs. CLTs separate property ownership from land ownership and assign the latter to non-profit organizations, which steward their affordability and land use over the long term. Residents can then democratically control the housing itself, whether individually or collectively as coop owners. CLT boards incorporate non-residents in their governance structure, slightly increasing their social equality ranking above limited equity cooperative models, like Mitchell Lamas. To be truly accessible to extremely low-income residents, CLTs need long-term government funding commitments for the part of operating expenses not covered by rent or maintenance charges.

Public Housing

Decommodification: High

Social equality: Low

Resident control: Middle

The New York City Housing Authority (NYCHA) is the largest public housing authority in the United States, housing about 400,000 people in 170,000 apartments. One in 15 New Yorkers live in public housing, supported by capital and operating assistance from the federal government and resident rents.

Public housing is among the most affordable in the U.S. housing system, because all tenants are charged 30 percent of their adjusted income as rent. It is also owned by governmental housing authorities with a mission to provide deeply affordable housing in perpetuity. This provides a buffer against commodification, as long as the authorities maintain their stewardship role. Unfortunately, underfunding by all levels of government has exposed the authorities to market pressure and led many of them to eliminate public housing or shift toward higher-income residents. NYCHA has mostly resisted this path, but now faces a $40 billion capital backlog.

Public housing ranks low on social equality because it is overwhelmingly occupied by low income tenants of color and is socially stigmatized and politically marginalized. Public housing residents are protected by strong federal provisions for resident organizing and other rights. However, the model’s resident control ranking is undercut by a suite of punitive policies aimed at exercising control over tenants, from citations for “lingering” to permanent exclusion from public housing grounds.

Mitchell-Lama Cooperatives

Decommodification: High

Social equality: Middle

Resident control: High

Active from 1955 to 1974, the Mitchell-Lama program was created to incentivize the development of cooperatives and rentals for moderate-income residents in New York State, incentivizing developers with below-market mortgages and tax exemptions in exchange for a limitation on profits and income targeting. There are about 61,000 Mitchell-Lama cooperative units in New York State in over 80 developments. Ten developments with 6,000 units have opted-out of the program since the 1990s.

Residents of Mitchell Lama limited-equity cooperatives enjoy most of the rights of other multifamily owner-occupants, including control over their length of tenure and building governance. Residents elect boards of directors, who then hire the management companies that run their properties. However, residents cannot sell their units on the open market, limiting the model’s speculative potential. As a result, it scores high on decommodification. The Mitchell-Lama program only guarantees temporary affordability, making the model more susceptible to privatization than public housing or community land trusts. However, owner-occupied Mitchell Lama cooperatives have been much less likely to opt out of their affordability requirements than developer-owned Mitchell-Lama rentals.

HDFC Cooperative

Decommodification: Medium

Social equality: High

Resident control: High

Housing Development Finance Corporation (HDFC) cooperatives are an affordable cooperative model. From the late 1960s to the 1990s, tenants and organizations like the Urban Homesteading Assistance Board (UHAB) converted many tax foreclosed, city-owned properties into HDFC coops, which enjoy reduced property taxes in exchange for resale restrictions.

Like Mitchell-Lama cooperatives, they score high on resident control. HDFC coops score lower than Mitchell-Lama coops on decommodification because HDFC owners can sell their apartments on an open market, but to an income-restricted pool of buyers. This creates more potential for speculation, as some apartments are sold at high prices to people with low incomes, but ample assets. Further, HDFC affordability contracts are temporary.

At the same time, because of their historical emergence in disinvested neighborhoods through tenant organizing, some HDFC coops continue to include more lower-income residents than Mitchell-Lama coops, extending the status and advantages of owner-occupancy to a broader portion of society. The model scores high on social equality.

Project-Based Section 8

Decommodification: Middle

Social equality: Low

Resident control: Middle

Active from 1974 to 1989, the federal project-based Section 8 program provides rental assistance to developers, filling the gap between 30 percent of a tenant’s monthly income and a formula-determined fair market rent. Most project-based Section 8 buildings also received federal mortgage financing for their development. There are about 45,000 project-based Section 8 apartments. About 9,000 have opted out since the 1990s.

Like public housing, project-based Section 8 rentals charge income-based rents and are affordable to tenants with the lowest incomes. Tenants are overwhelmingly low-income people of color, and are often socially stigmatized and politically marginalized.

Project-based Section 8 rentals score lower than public housing on decommodification, because they are temporarily affordable under a federal agreement with a private owner. Both for-profit and nonprofit entities own project-based Section 8 housing, and at contract expiration, ownership type has an impact on whether or not the property opts out of affordability. Non-profit project-based Section 8 rentals score slightly higher on decommodification than their market counterparts as a result.

Project-based Section 8 rentals score higher than unsubsidized rentals on resident control, because the model incorporates a high level of resident rights, including the right to organize, protections from landlord reprisal, and opt-out/property sale notification requirements.

Mitchell-Lama Rental

Decommodification: Middle

Social equality: High

Resident control: Middle

Active from 1955 to 1974, the Mitchell-Lama program was created to incentivize the development of cooperatives and rentals for moderate-income residents in New York State, incentivizing developers with below-market mortgages and tax exemptions in exchange for a limitation on profits and income targeting. There are about 32,000 Mitchell-Lama rental units in New York State. Over 33,000 units have opted-out of the program since the 1990s.

Today, Mitchell-Lama rentals are supported by a variety of subsidies. Some residents pay income-based rents; others pay regulated rents based on the cost of operating the housing, plus mortgage payments and a limited profit to owners. As a result, tenants have a wider range of incomes than in other forms of subsidized housing, and Mitchell-Lama rentals are generally not strongly stigmatized, making this one of the more socially egalitarian forms of housing in the United States.

Mitchell-Lama rentals score in the middle on decommodification because like other forms of private subsidized housing, they are temporarily affordable. At the same time, Mitchell-Lama rentals have some of the strongest tenant associations in New York City, perhaps because of strongly defined resident rights under the program, including tenants’ recognized role in reviewing owners’ rent increase applications. These organizations often successfully exercise control over their property, like the tenants in Atlantic Plaza Towers who recently successfully defeated their landlord’s plan to install invasive facial recognition technology in their development.

Low Income Housing Tax Credit Rentals

Decommodification: Middle

Social equality: Middle

Resident control: Middle

Created in 1986, the federal Low Income Housing Tax Credit (LIHTC) is a time-limited tax incentive that functions like a capital subsidy by facilitating private investment in affordable housing. In a LIHTC deal, developers receive tax credits from the city or state for a specific affordable housing project and then transfer those credits to investors. Developers use the proceeds to build/rehabilitate the housing, while the investors reduce their tax obligations. The 2017 tax overhaul, which dramatically lowered the corporate tax rate, undercut LIHTC value. There are over 100,000 apartments supported by LIHTC in New York City, but there is overlap between LIHTC and Mitchell-Lama rental, project-based Section 8, and rent regulated housing.

Rental buildings developed with the federal Low Income Housing Tax Credit (LIHTC) are the centerpiece of the Bloomberg and de Blasio affordable housing plans, because LIHTC is the largest federal program for new affordable housing production and preservation. Like other forms of private subsidized housing programs, LIHTC offers temporary affordability. This results in privatization pressure at contract expiration, a problem that will become more acute in the next few years in New York as more LIHTC properties will begin to expire. As with project-based Section 8, for-profit versus nonprofit ownership has an impact on whether or not properties opt out of affordability. National HUD research has shown that non-profit developers are more likely to renew their LIHTC contracts than for-profit developers.

LIHTC rentals score in the middle on resident control. LIHTC tenants generally have similar rights to other subsidized renters, but they are often less aware of them (and less organized as a tenant class) because the program has fewer tenant notification requirements.

Rent Regulated Rental

Decommodification: Middle

Social equality: Middle

Resident control: Middle

Rent regulation laws are designed to correct the power imbalance between landlords and tenants. There are nearly a million rent regulated apartments in New York City, accounting for 45 percent of the rental housing stock. More low-income households (365,000) live in rent regulated apartments than in any other type of housing. Regulated rentals score higher on decommodification than other private unsubsidized rentals because controlled rent increases lower their speculative potential. Strengthened rent laws under the Housing Stability and Tenant Protection Act of 2019 should further stabilize rent regulated property values. The elimination of the vacancy bonus, caps on individual apartment improvements, and preferential rent reform mean that landlords can no longer project rapid increases in their rent rolls that greatly exceed annual Rent Guidelines Board adjustments, and then take on mortgage debt based on those projections.

While rent regulation is not a housing subsidy, rent regulated renters have the greatest protections among private market tenants, creating an opportunity for a medium level of resident control. Limits on rent increases give tenants the ability to organize with less fear of landlord retaliation.

Market Rental

Decommodification: Low

Social equality: Middle

Resident control: Low

There are 937,000 market rental apartments accounting for 43 percent of the rental housing stock. Market rate multifamily rental buildings are generally owned by landlords seeking to maximize the return on their investments, and are thus most dominated by market considerations. Owners have relatively few restrictions on property disposition. The model scores lower than owner-occupied homes on decommodification.

While unregulated renters have some rights under state law–recently expanded by the Housing Stability and Tenant Protection Act of 2019–they still have very limited control over their homes. Residents generally do not have the right to a lease renewal or protections against punitive rent hikes, severely limiting their ability to organize. Residents of month to month rentals and other non-lease living arrangements have even fewer rights.

Investment Property

Decommodification: Low

Social equality: Low

Resident control: Low

Investor ownership is a growing trend in New York City, impacting both the luxury real estate market, as well as lower-priced starter homes. Research by the community group Chhaya has shown that the share of non-owner occupied one to four family homes in Queens doubled over the last decade.

Non-owner occupied single-family houses and condos have a higher speculative value than owner-occupied homes, because of an implicit commitment to a maximum return on investment and the lack of restrictions on property disposition. Lending practices for these properties assume a higher level of risk, making them more prone to speculative practices like flipping and over-leveraging. If investment properties are offered up for rent, tenants generally do not have the right to a lease renewal or protections against punitive rent hikes, severely limiting their ability to organize.

Homeless Shelters

Decommodification: Low

Social equality: Low

Resident control: Low

There were 78,604 homeless people in New York City in 2019, including those living in municipal and private shelters, hotels and cluster sites, and sleeping on the street. The current administration has been expanding shelter capacity to address rapidly growing homelessness in the city. Advocates have called for permanent housing solutions, recently winning a required 15 percent set aside in new subsidized developments.

Public and private shelters score the lowest on the resident control scale because residents are subject to a high level of surveillance and have minimal control over their duration of stay or their housing location. People living within the shelter system have minimal avenues for recourse over conditions or ability to organize, and are also among the most stigmatized people in all of society.

Private shelters score low on decommodification because they are also subject to conversion for other uses, if the potential to do so profitably arises.

New York State housing advocates are calling for an expansion of the social housing sector in the state, including increased funding for public and supportive housing and a new Tenant Opportunity to Purchase (TOPA) law, which would allow tenants to buy their buildings if they go up for sale or into foreclosure (watch this blog for an analysis of TOPA soon). These immediate policy solutions are part of a longer-term strategy to redefine housing as a vital public good. Our analysis shows that New York State has a vast framework for a robust social housing sector; what is required are the resources and political will to realize this vision.

Did you miss part 1 of our series? Read more about social housing in the U.S. here.

The authors thank Ryan Acuff, Celeste Hornbach, Karen Narefsky, Tara Raghuveer, and Cea Weaver for speaking to us for this piece.

![]()