Explaining the Trouble in Multifamily Finance: Landlords Bet Big on Displacement, and Now Seek Government Relief in the Form of Rising Rents

Oksana MironovaSamuel SteinCeleste HornbachJacob Udell

Over the past two years, we have seen the value of some rent stabilized properties decline and the collapse of one of the major lenders to rent stabilized landlords, Signature Bank. This precipitated a first-of-its-kind federal rescue plan of a $15 billion multifamily building portfolio. Meanwhile, New York Community Bank (NYCB)—long a target of community development organizations for its exploitive lending practices— seems to be facing similar troubles.

This instability is the result of many years of risky, predatory, and— for a time—tremendously profitable financial practices on the part of landlords and their lenders.

How Did Rent Stabilized Buildings Get So Expensive?

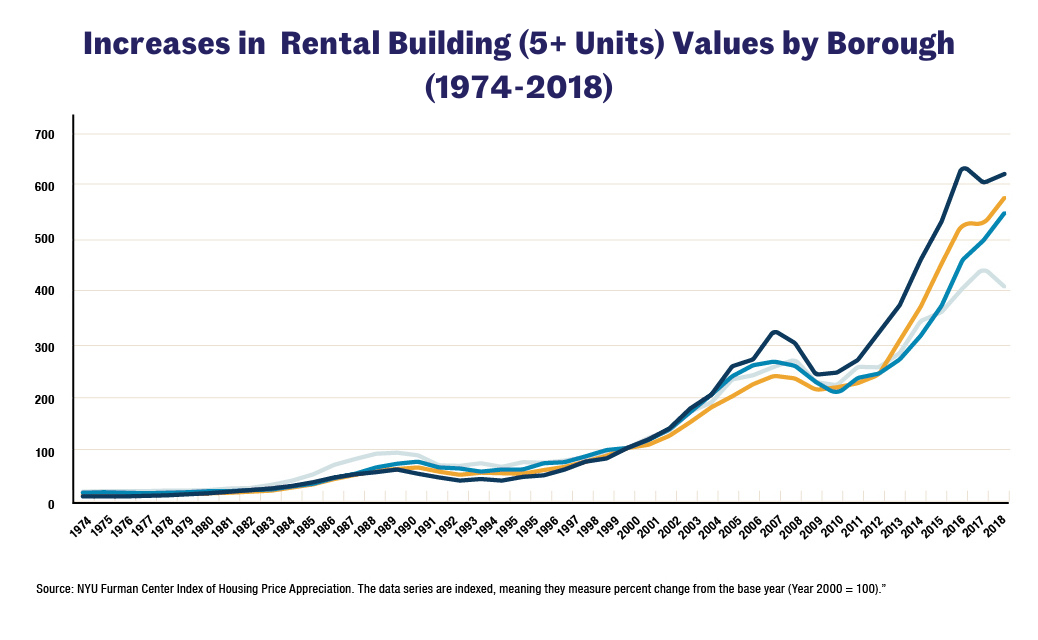

Rental building values have risen in two waves since the mid-1990s. The first wave occurred between 1995 and 2007, when the average annual rental building sales price in New York City increased by almost 400 percent in every borough except Staten Island. Between 2010 and 2018, median sales prices for rental buildings rose again, more than doubling in many neighborhoods.

In Upper Manhattan, the Bronx, Brooklyn, and Queens, total sales volume for rentals rose from $1.28 billion in 2010 to a high point of $8.31 billion in 2016.

Average debt levels per unit in NYC (excepting SI) rose 121% between 2010 and 2018.

Overleveraging and Displacement as a Business Practice

Over the past 25 years, landlords have been rewarded handsomely for treating their buildings as commodities, while tenants have continued to struggle for recognition that these buildings are not just investment vehicles but homes.

Selling a building for more than the purchase price is the most direct, but not the most common way landlords make money of their buildings in New York. Landlords generate major profits by increasing a building’s net operating income (NOI) by hiking up rents or by spending less money on operations. Both come at tenants’ expense: increasing rents displaces long-term tenants, while cutting operating expenditures creates disrepair.

The astronomical rise of property values over the last 25 years created the conditions for landlords to seize on a third way of generating massive profits: by increasing the size of the mortgages carried by their buildings.

Just how big a mortgage a lender is willing to extend to a landlord depends on the building’s NOI. When a building’s NOI goes up, either because of increased rents or decreased services, a landlord can go back to their lender—like Signature or NYCB—and refinance their building’s mortgage for a higher amount. As the Association for Neighborhood and Housing Development’s (ANHD) Equitable Reinvestment Committee (ERC) has shown, some multifamily lenders’ core business practices relied on “making multifamily loans to bad acting landlords.” For example, “year after year, building after building, Signature consistently made multifamily loans that were speculative and underwritten to practices of displacement, harassment, or building neglect.”

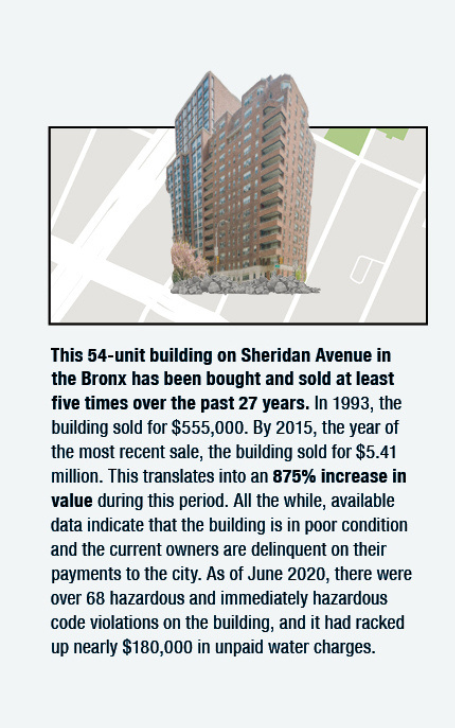

Once a landlord is approved for a larger mortgage, they can keep the difference between what they originally paid for a building and the larger mortgage; the real estate industry term for this is “pulling out equity.” If the building’s value rises dramatically, the landlord can both recoup their down payment and turn the difference between the building’s original value and its increased value into profit.

Landlords do not have any obligation to use this debt-generated profit to improve their existing buildings and make living conditions better for their tenants. As CSS’s Unheard Third survey has shown over and over again, there is no direct relationship between rising rents and improved conditions for tenants. Instead of putting money into the building, landlords often use the money to buy more rental buildings, or as cash payouts to themselves or their investors.

What does HSTPA Have to Do with It?

The Housing Stability and Tenant Protection Act (HSTPA) of 2019 made it more difficult for landlords to employ unscrupulous NOI-raising strategies that encourage maintenance deferral and displace long-term tenants in over one million rent stabilized units. Before the HSTPA, when a tenant moved out, rent stabilized apartments were eligible for a 20 percent as-of-right increase and unchecked and often inflated increases resulting from Individual Apartment Improvements. Apartments that reached a legal rent of $2,816 were eligible for decontrol. Unscrupulous landlords developed business practices contingent on these loopholes, all geared toward increasing the NOI of their stabilized properties, which allowed them to overleverage their buildings with more and more debt. Conditions for tenants got so bad that the city and state were forced to sharpen their definitions of tenant harassment.

If rent stabilized building values are now falling, it’s because the market is resetting to the prices associated with the rents in the buildings – no more, no less. If previous rounds of sky-high valuations were based on dreams of ever-rising rents and NOI, today’s are based on realistic assessments of what tenants pay each month according to the law.

The city and state need to step up and turn distressed rent stabilized properties into social housing

The HSTPA reined in the worst of these speculative practices, shifting the power relationship between landlords and their tenants. Unscrupulous landlords and lenders bet on displacement and tenant harassment as business practice and lost.

It is not New York State’s responsibility to reward decades of bad behavior with a rescue plan that will hurt tenants.

At the same time, there are distressed rent stabilized properties on the market. This is an opportunity for the city and state to rescue these properties and turn them into permanently affordable housing. The city could intervene by funding Neighborhood Pillars, a program created by the de Blasio administration in the long shadow of the 2008 foreclosure crisis. Neighborhood Pillars provides financing to qualified non-profit housing providers to purchase distressed rent stabilized apartments and run them as permanently affordable housing. While the program is currently paused, a new push from the agency and a budgetary expansion could jumpstart this program and buy out any underwater rent stabilized landlords who are ready to part with their buildings.

Other proposed legislation, including the Tenant Opportunity to Purchase Act (S221/A3353) and the Social Housing Development Authority (S8494/A9088) at the state level and the Community Opportunity to Purchase Act (Int 1977) at the City level could also facilitate transfers from distressed private ownership to public, tenant community-controlled social housing.